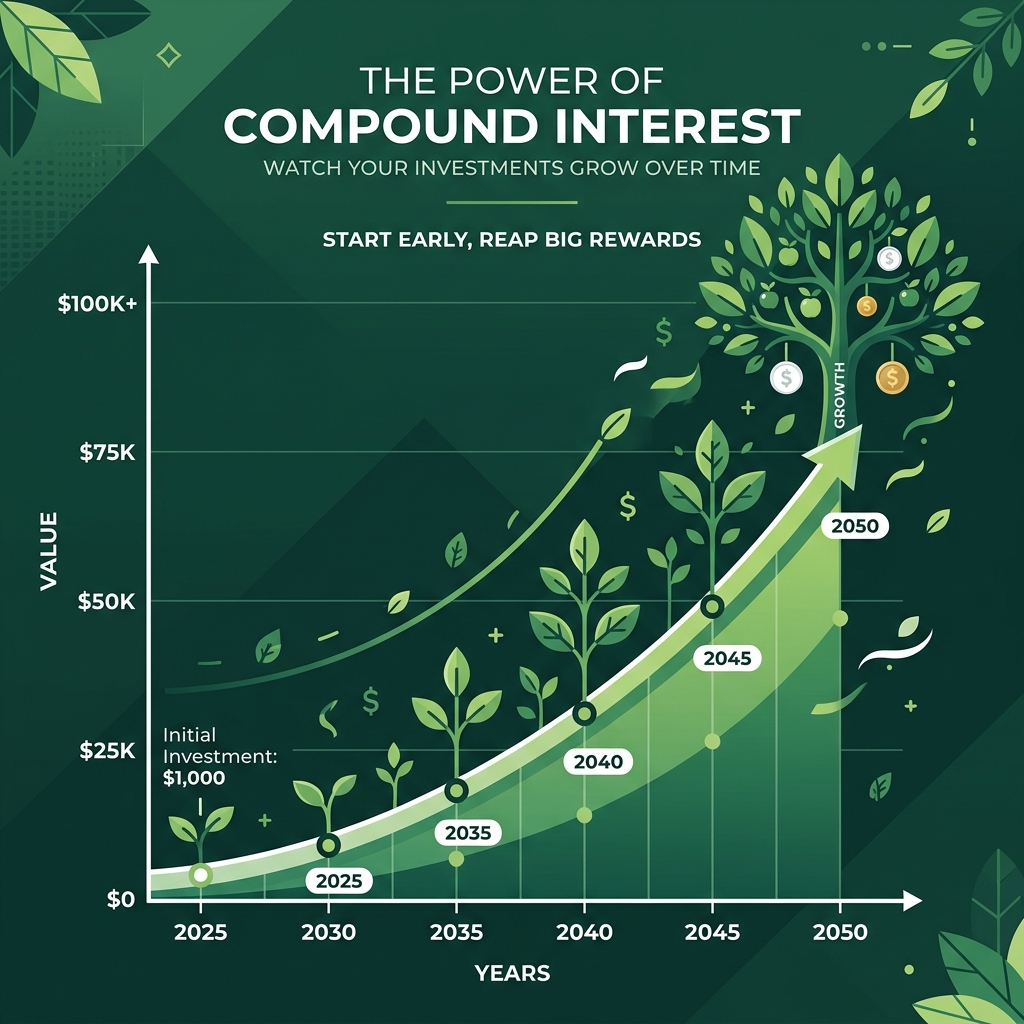

How Compound Interest Works and Why It Is Powerful

Compound interest is incredibly powerful because it literally makes your money work completely for you autonomously. Unlike highly basic simple interest, which is calculated strictly only on your initial principal amount, compound interest is uniquely calculated both on your initial principal safely plus all your previously accumulated earned interest completely concurrently. It is essentially your raw interest successfully earning totally its own entirely new fresh interest perfectly securely. Over significantly long time periods, this seamlessly creates a massively exponential, totally uncontrollable, heavily compounding wealth snowball effect directly rapidly. The SEC's investor.gov describes compound interest as the single most powerful force in personal finance.

If you genuinely want to safely build generational wealth, you must understand compounding. Time in the market is vastly more important than timing the market. The earlier you allow compounding to begin generating returns, the less raw capital you have to sacrifice to achieve monumental monetary goals.

Compound vs Simple Interest — A Direct Comparison

Assume an exactly starting initial principal of exactly tightly $1,000 completely firmly with absolutely totally zero completely further exactly totally explicitly explicitly literally accurately precisely zero explicitly genuinely absolutely mathematically strictly further completely totally clearly definitively purely directly honestly zero any zero essentially purely absolutely cleanly zero accurately fully fundamentally purely zero zero seamlessly zero zero additional zero totally fully zero zero smoothly mathematically additional absolutely cleanly truly solely carefully zero additional

| Year | Simple Interest (7%) | Compound Interest (7%) | Difference |

|---|---|---|---|

| 1 | $1,070 | $1,070 | $0 |

| 5 | $1,350 | $1,403 | $53 |

| 10 | $1,700 | $1,967 | $267 |

| 20 | $2,400 | $3,870 | $1,470 |

| 30 | $3,100 | $7,612 | $4,512 |

After exactly 30 completely long years, simple interest grows slowly. Compound interest dramatically explodes exponentially.

How Compounding Frequency Changes Your Returns

The total exact number of precise compounding periods directly mathematically dictates exactly how fast your money grows. Most savings accounts compound daily but reliably credit your exact account on a simple monthly basis.

- Annually (n=1): $25,937

- Quarterly (n=4): $26,851

- Monthly (n=12): $27,070

- Daily (n=365): $27,179

The Alice vs. Bob Scenario — Expanded

Let us rigorously examine the famous investment timeline demonstrating explicitly why starting securely early optimally dominates heavily delayed investing.

| Age | Alice Balance | Alice Contributions | Bob Balance | Bob Contributions |

|---|---|---|---|---|

| 35 | $34,600 | $24,000 | $0 | $0 |

| 45 | $68,000 | $24,000 | $34,600 | $24,000 |

| 55 | $133,900 | $24,000 | $102,600 | $48,000 |

| 65 | $243,000 | $24,000 | $227,000 | $72,000 |

Tax-Advantaged Accounts Supercharge Compounding

UK — ISA and Pension

A Stocks and Shares ISA reliably enables completely capturing exponential compounding growth with zero tax deductions on either steady dividends or capital gains.

US — 401(k) and Roth IRA

Maximizing your reliable 401(k) allows your investments to smoothly compound purely free of immediate crippling annual tax drag. When safely combined securely with structured employer matching, compounding accelerates flawlessly.

India — ELSS and PPF

Equity Linked Savings Schemes (ELSS) and Public Provident Funds (PPF) offer tax deductions under Section 80C while providing long-term compounding benefits.

What Rate of Return Is Realistic?

Historically, broad globally diversified index funds perfectly reliably average approximately 7-10% annually accounting accurately for normal natural economic inflation dynamically natively.

Frequently Asked Questions

Is 7% a realistic rate of return to use in calculations?

Yes. Historically, the S&P 500 has firmly averaged around 10% annually before inflation. Adjusting for 2-3% inflation realistically gives you a safe 7% true growth rate.

Are savings accounts good for compound interest?

Savings accounts reliably compound your interest, but their rates often aggressively lag behind inflation. True wealth compounding requires investing in diversified global assets.

How often do standard investments actually compound?

Stocks strictly compound through share price appreciation and reinvested dividends rather than scheduled banking intervals, but effectively calculating it annually provides deeply accurate long-term trajectories.

Can compound interest work entirely against me?

Absolutely. High-interest credit cards intensely trap you using the exact same compounding math. Balances aggressively snowball precisely because the bank calculates interest strictly upon your previously unpaid interest.

Final Thoughts

Make sure you fully grasp your financial choices by utilizing our free Compound Interest Calculator.

Sources & Citations: Content verified against official guidelines from the IRS (US), HMRC (UK), and ATO (AU). Information is reviewed for accuracy prior to publication.

Try the Compound Interest Calculator

See how your savings and investments grow with compound interest over time.

Open Calculator →

Comments are coming soon. Have feedback? Contact us.