Understanding Basic Mortgages for First Time Buyers

A mortgage is essentially a massive loan explicitly used to purchase physical property or land. The property itself safely serves as direct collateral for the loan. This means the specific lender retains the strict legal right to forcefully take possession of your home if you fail to sustainably make your agreed payments. This formal legal process is known as foreclosure in the US or repossession in the UK. Understanding precisely how mortgages mechanically work is absolutely crucial for successfully navigating one of the realistically largest financial decisions you will carefully effectively make.

How a Mortgage Actually Works — The Maths

Let us thoroughly break down a simple real-world worked numerical example to clearly illustrate the exact costs.

- Home price: $300,000

- Down payment: 20% = $60,000

- Loan amount: $240,000

- Interest rate: 6.5% fixed strictly for exactly 30 years

- Monthly basic payment: Approximately $1,517 (covering solely just principal plus interest)

Over the full unyielding 30 years, your total combined payments massively amount to roughly $546,120. Astonishingly, you end up paying $306,120 in pure bank interest alone. This accurately means you practically pay significantly more strictly in raw interest than the original sticker price of the home itself. This stark reality profoundly highlights exactly why making extra principal payments and fiercely securing slightly lower rates desperately matters so heavily to your ultimate long-term wealth.

What Exactly Makes Up Your True Monthly Payment?

Your actual monthly payment invariably includes four distinct heavy components (commonly abbreviated as PITI):

- Principal: The pure physical portion that directly structurally reduces your total outstanding original loan balance.

- Interest: The massive pure strict cost heavily charged by the bank simply for borrowing their money.

- Taxes: Required property taxes, which the strict lender usually forcefully holds perfectly safely in a dedicated escrow account.

- Insurance: Essential homeowners insurance and highly expensive Private Mortgage Insurance (PMI) if legally applicable.

Fixed vs Adjustable Rate — When Each Makes Sense

Choosing explicitly between fixed and explicitly adjustable rate products heavily dictates your future strict exact monthly liability.

| Crucial Factor | Standard Fixed Rate Product | Standard Adjustable Rate (ARM) |

|---|---|---|

| Initial rate | Generally slightly higher safe starting rate | Visibly lower starting introductory 'teaser' rate |

| Payment stability | Perfectly legally predictable securely for life | Blindly changes drastically after strict fixed period ends |

| Best for | Committed buyers strictly staying happily 5+ years | Strictly strictly short-term temporary ownership plans |

| Risk profile | Slightly missing out if market rates heavily heavily drop | Massive intense payment shock when temporary rates strongly reset |

| Current Example | Typically 6.5% - 7.0% (US 2024 Market) | Roughly 5.5% - 6.0% pure initial strict lock (US 2024) |

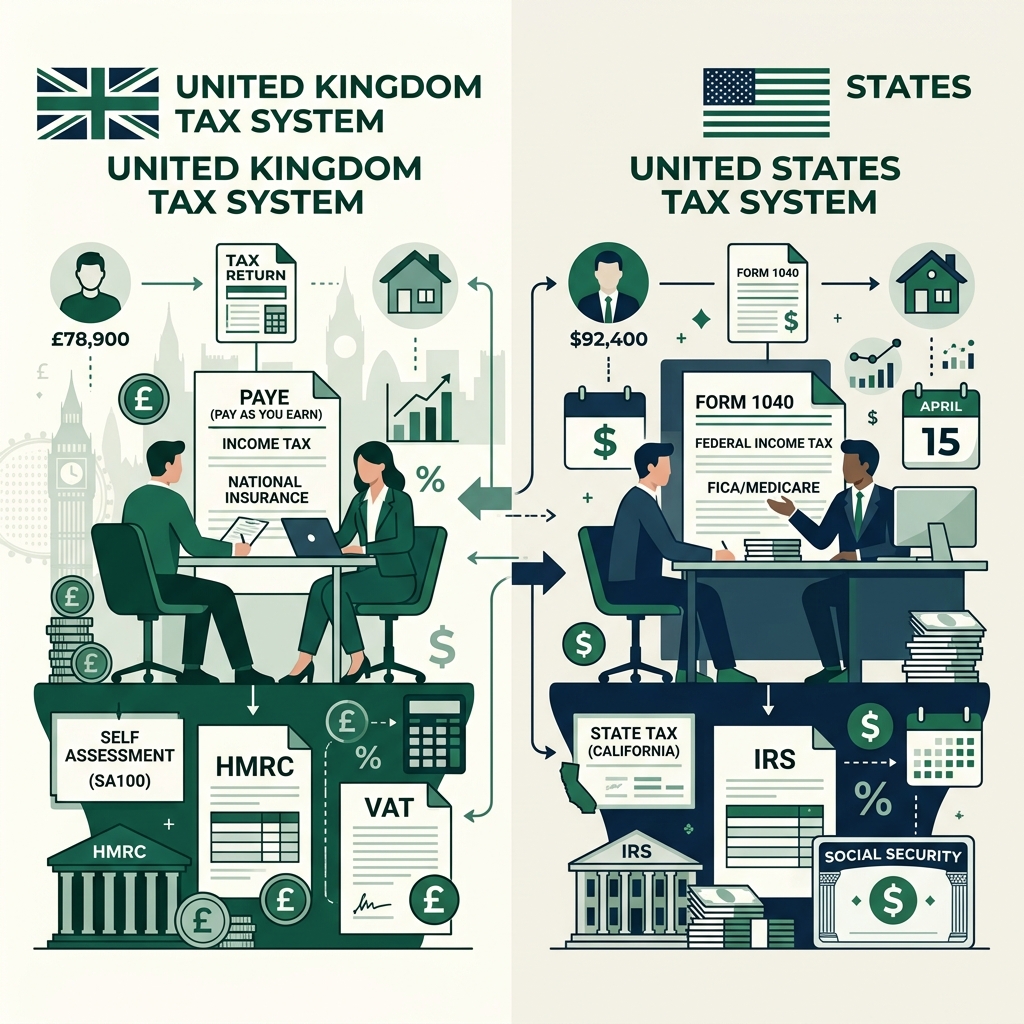

UK vs US Mortgage Differences

The Unique UK Mortgage Market

Most standard UK mortgages are fixed-rate products for an initial 2 or 5-year period, after which the rate reverts to the lender's Standard Variable Rate (SVR). The UK mortgage market is regulated by the Financial Conduct Authority (FCA).

After the fixed term ends, UK homeowners typically remortgage to a new deal to avoid the higher SVR. Failing to remortgage can add hundreds of pounds to your monthly payment.

The Standard US Mortgage Market

The standard US mortgage is a 30-year fixed-rate loan, though 15-year products are popular for buyers who want to build equity faster and pay significantly less total interest.

FHA loans (backed by the Federal Housing Administration) allow down payments as low as 3.5% for buyers with credit scores of 580 or above, making homeownership accessible to first-time buyers with limited savings.

Your Exact Credit Score and Formal Mortgage Rates

Here is how your credit score directly impacts the mortgage rate you are offered on a $300,000 30-year loan. The Consumer Financial Protection Bureau (CFPB) recommends checking and improving your score at least 6 months before applying.

| Your Credit Score | Approximate Current US Rate | Monthly Formal Payment (P&I) |

|---|---|---|

| 760 - 850 | 6.2% | $1,835 |

| 700 - 759 | 6.4% | $1,872 |

| 640 - 699 | 6.9% | $1,975 |

| 580 - 639 | 7.5% | $2,098 |

The True Absolute Cost of Buying — Way Beyond the Mortgage

The true cost of buying a property extends far beyond the mortgage. Budget for these additional one-time costs:

- Solicitor / conveyancing fees: £1,500 – £3,000 (UK) or closing costs 2–5% of loan value (US)

- Survey / home inspection: £300 – £1,500 (UK) or $300 – $500 (US)

Frequently Asked Questions

What exactly is a good down payment amount?

While 20% historically strictly eliminates costly mortgage insurance entirely, many first-time buyer formal programs happily accept solidly legally secure down payments as low as 3% to 5%.

Can I aggressively pay my mortgage early?

Yes. Most modern mortgages allow for extra principal payments without any penalty, which dramatically reduces your total interest paid.

What specifically is PMI?

Private Mortgage Insurance protects the lender in case you default. It is usually required if you put down less than 20%.

Should I use an adjustable-rate mortgage?

Only if you are absolutely certain you will sell the home or refinance before the fixed introductory period ends. Otherwise, the rate increases can cause payment shock.

Final Thoughts

Make sure you fully grasp your financial choices by utilizing our free Compound Interest Calculator.

Sources & Citations: Content verified against official guidelines from the IRS (US), HMRC (UK), and ATO (AU). Information is reviewed for accuracy prior to publication.

Try the Compound Interest Calculator

See how your savings and investments grow with compound interest over time.

Open Calculator →

Comments are coming soon. Have feedback? Contact us.